A New Blueprint for Digital Money: Where Privacy Meets Compliance

There’s a quiet shift happening in the architecture of money—and it starts with a familiar frustration.

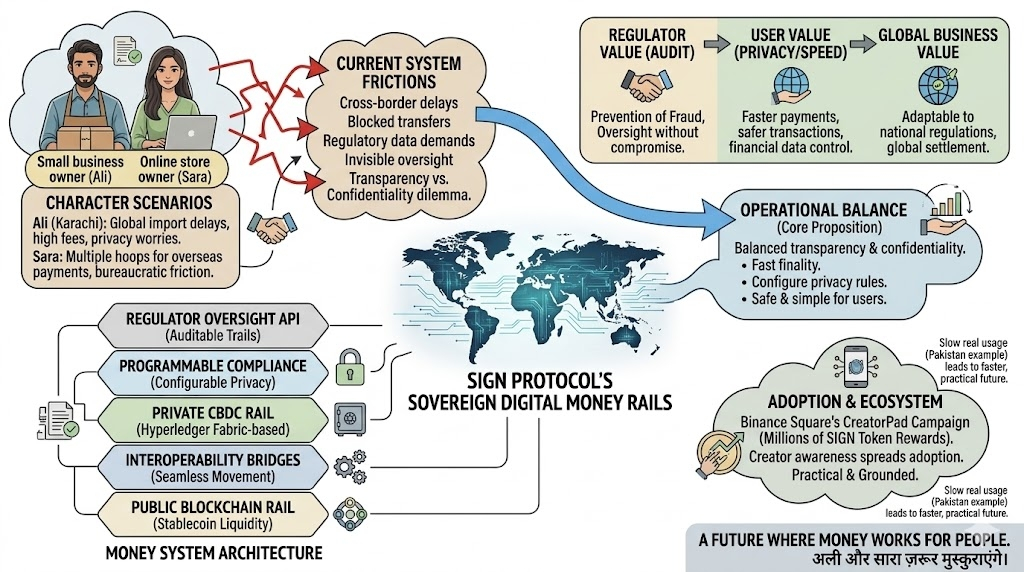

Last week, a conversation with Ali, a small business owner in Karachi, exposed a crack in the global financial system that millions know all too well. Cross-border payments remain painfully inefficient: sluggish settlement times, unpredictable blocks, and fees that erode already-thin margins. For entrepreneurs operating in emerging markets, the system isn’t just outdated—it’s restrictive.

But speed isn’t the only concern. Privacy sits on the other side of the scale. As financial systems become more digitized, surveillance increases. Documentation demands grow. Transparency, while necessary for compliance, often comes at the cost of personal financial autonomy.

This is the paradox of modern finance:

How do you build a system that is fast, compliant, and private—without compromising any of the three?

The Transparency–Privacy Tradeoff

Ali’s story echoes globally. So does Sara’s—an e-commerce operator who recently spent hours navigating bureaucratic friction just to complete a simple overseas payment. These aren’t edge cases. They are symptoms of a system caught between two opposing forces:

- Regulators demand visibility to prevent fraud and ensure compliance

- Users demand privacy and efficiency in their financial lives

Traditional systems force a tradeoff. You either get speed without privacy, or privacy without auditability.

But what if that tradeoff is no longer necessary?

Enter the Dual-Rail Model

This is where Sign Protocol’s “New Money System” introduces a compelling shift—not as just another cryptocurrency, but as an infrastructure layer designed for real-world financial complexity.

At its core is a dual-rail architecture:

- A public blockchain layer optimized for transparency, cross-border payments, and corporate use cases

- A private, permissioned blockchain tailored for sensitive financial activity, such as central bank digital currencies (CBDCs)

On the private rail, transactions remain confidential by default. Yet, crucially, they are selectively accessible to regulators when required. This isn’t anonymity—it’s programmable privacy.

Seamless Value Transfer

What makes the system particularly elegant is how these two rails interact.

Through integrated bridges, assets can move fluidly between private and public environments. Imagine this flow:

- A transaction originates within a private CBDC system

- It transitions into a stablecoin on the public chain for cross-border settlement

- It reaches its destination almost instantly—without exposing sensitive user data

The complexity is abstracted away. For users like Ali, it simply feels like money moving at the speed of the internet.

Built for Scale, Designed for Control

Under the hood, the system leverages Hyperledger Fabric-based infrastructure, enabling:

- Configurable privacy controls

- High-speed transaction finality

- Strong governance frameworks

This architecture proves a critical point: privacy and scalability are not mutually exclusive. High-volume financial systems can remain both compliant and confidential.

Real-World Impact

For users, the value proposition is straightforward:

- Faster payments

- Reduced friction

- Greater control over personal financial data

For regulators:

- Built-in auditability

- On-demand visibility

- Policy-level programmability

It’s a rare alignment of incentives—where both sides of the financial equation benefit.

Ecosystem Momentum

Beyond infrastructure, ecosystem growth is already underway. Platforms like Binance Square are accelerating awareness through initiatives such as CreatorPad, offering token incentives to onboard and educate users.

This matters. Adoption in crypto doesn’t just come from technology—it comes from accessibility and participation. When users like Ali and Sara can engage, learn, and benefit early, the system becomes more than theoretical.

The Bigger Picture

What Sign Protocol hints at is larger than a single product—it’s a rethinking of how nations might approach digital money altogether.

- Payments become invisible and instant

- Compliance becomes embedded, not enforced

- Privacy becomes a feature, not a vulnerability

If successful, this model could mark a turning point: where digital finance stops feeling experimental—and starts feeling human.

The next time a payment stalls or a transaction gets buried in red tape, it’s worth remembering: the foundations of a new financial system are already being built.

One where money finally works the way it should.